Colossus (51 page)

There is one other, more drastic possibility, however. Bond markets worry about default on the government’s explicit, tradable liabilities, not its implicit liabilities such as Social Security. A default on the government’s nontradable liabilities may seem hard to imagine, but it has a historical precedent. In

ancien régime

France the biggest burden on royal finances did not take the form of bonds but the salaries due to tens of thousands of officeholders, men who had simply bought government sinecures and expected in return to be paid salaries for life. All attempts to reduce these implicit liabilities within the existing political system simply failed. It was only after the outbreak of the Revolution—arguably a direct consequence of the fiscal crisis of the monarchy—that the offices were abolished. The officeholders were compensated by cash payments in a new currency, the

assignats

, which within a few years were reduced to worthlessness by the revolutionary printing presses.

49

Vested interests that resist necessary fiscal reforms can end up losing much more heavily from a revolutionary solution.

Perhaps, then, Paul Kennedy was not so wrong to draw parallels between modern America and prerevolutionary France. Bourbon France, like America today, had pretensions to imperial grandeur but was ultimately wrecked by a curious kind of overstretch. It was not their overseas

adventures that did it for the Bourbons. Indeed, Louis XVI’s last foreign war, in support of the rebellious American colonists, was a huge strategic success. The French overstretch was internal, and at its very heart was a black hole of implicit liabilities. In the same way, the decline and fall of America’s undeclared empire may be due not to terrorists at the gates or to the rogue regimes that sponsor them, but to a fiscal crisis of the welfare state at home.

This fiscal crisis is not of course a problem unique to America. It afflicts the world’s second- and third-largest economies even more seriously. But neither Japan nor Germany any longer has pretensions to be a global hegemon, so their decline into economic old age has minimal strategic implications. That is not true in the American case. As Gibbon said, the finances of a declining empire do indeed make an interesting subject.

THE DEBTOR EMPIRE

Yet the extent of the fiscal problems of the United States and the timing of their manifestation cannot be discussed with reference to American expectations alone. This is a world of globalized capital flows, and no American foreign policy initiative can be divorced from one crucial fact: that this is a debtor empire.

It is an unusual, though not unprecedented, state of affairs. In the heyday of the European empires, the dominant power was supposed to be a creditor, investing a large proportion of its own savings in the economic development of its colonies. Hegemony, in short, also meant hege

money

. When the last great Anglophone empire bestrode the globe a hundred years ago, capital export was one of the foundations of its power. Between 1870 and 1914 net flows out of London averaged between 4 and 5 percent of gross domestic product; at their peak on the eve of the First World War they reached an astonishing 9 percent. This was not merely an extraordinary diversion of British savings away from home. It was also a remarkable attempt to transform the global economy by investing in the construction of commercial infrastructure—docks, railways and telegraph lines—in what we would now call less developed countries. Whatever its undoubted

shortcomings in other respects, one undeniable benefit of British hegemony was that it encouraged investors to risk their money in such countries, something they are significantly less willing to do in our own time.

This was not just a British idiosyncrasy. When the United States was fitfully asserting itself in Central America, the Caribbean, Europe and Asia in the first half of the twentieth century, it was able to engage in “dollar diplomacy” because it was a substantial net capital exporter. By 1938 the gross value of U.S. assets abroad amounted to $11.5 billion.

50

Having bankrolled the victors during both world wars, the United States bankrolled the reconstruction of the losers in peacetime too. The most famous example of U.S. capital export was, as we have seen, the Marshall Plan, the high watermark of official unrequited transfers to foreign governments. However, private American foreign lending continued to fuel the world’s economic recovery for a further two decades. Between 1960 and 1976 the United States ran current account surpluses totaling nearly $60 billion.

Those days are gone. Today, even as it boldly overthrows one rogue regime after another, the United States is the world’s biggest borrower. Since 1982 the country has run a current account deficit totaling nearly $3 trillion. In 2002 the deficit was 4.8 percent of GDP; in 2003 it was even higher.

51

According to one estimate, gross foreign claims on the United States in 2003 amounted to around $8 trillion of U.S. financial assets, including 13 percent of all stocks and 24 percent of corporate bonds. The country’s international investment position has changed dramatically, from net assets equivalent to 13 percent of GDP in 1980 to net liabilities worth 23 percent in 2002. In March 2003 the

Wall Street Journal

posed the question: “Is the U.S. hooked on foreign capital?”

52

The answer is yes, and it applies to the government even more than to the private sector. According to the Federal Reserve’s September 2003 estimate, foreign investors currently hold around 46 percent of the federal debt in private hands—more than double the proportion they held ten years ago.

53

These are extraordinary levels of external indebtedness, more commonly associated with emerging markets than empires. Indeed, Brazil’s net international indebtedness is now lower than that of the United States. At a press conference in April 2003, the International Monetary Fund chief economist Ken Rogoff remarked that he would be “pretty concerned” about “a developing country that had

gaping current account deficits year after year, as far as the eye can see, of five percent or more, with budget ink spinning from black into red, with the likely deficit to GDP ratio for general government exceeding five percent this year [and] open-ended security costs.” Of course, he hastily added, the United States is “not an emerging market.” But “at least a little bit of that calculus still applies.”

54

Perhaps more than a little.

Given that domestic political gridlock will surely lead to a stream of deficits in the coming decades, a great deal depends on whether or not foreign investors will be willing to absorb increasing quantities of U.S. treasuries. According to one line of argument, there is nothing to worry about on this score. The reason that so much overseas capital flows into the United States, so it is said, is that the American economy is the engine of global growth and foreign investors simply want a “piece of the action.” Yet foreign investors seem willing to settle for markedly lower returns when they invest in the United States than the returns Americans get when they invest overseas.

55

Far from acquiring equity in America’s dynamic corporations, many foreign investors turn out to be mainly interested in buying government bonds. Why is this? The explanation lies in the fact that a substantial and rising share of the foreign holdings of American bonds are in fact in the hands of East Asian central banks, which have been buying up dollar assets in order to keep their own currencies from appreciating against the dollar. Between April 2002 and August 2003 the central banks of China and Hong Kong bought ninety-six billion dollars of U.S. government securities.

56

The Bank of Japan was equally active.

From a strictly economic point of view, this may give no grounds for anxiety since the Asian central banks have as strong an interest in the arrangement as the big borrower itself. China’s exports to the United States are one of its principal engines of growth and job creation. Looked at another way, there is a neat symmetry between the American propensity to consume and the Chinese propensity to save. As

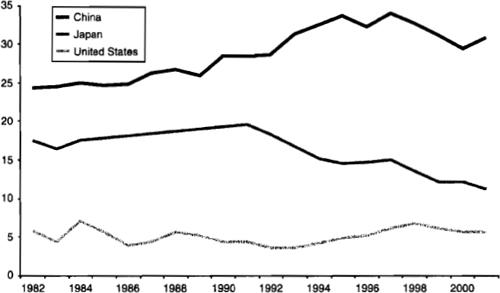

figure 13

shows, China is essentially playing the role that Japan played in the 1980s, channeling its surplus savings into the American current account and fiscal deficits. But what are the strategic implications of the fact that for its economic stability—to be precise, for its ability to finance federal borrowing at around 4 percent per annum—the United States is reliant on the central bank of the People’s Republic of China?

FIGURE 13

Net National Savings as a Percentage of Gross National Income, China, Japan and the United States, 1982–2001

Source: World Bank,

World Development Indicators

database.

There are two ways of thinking about this symbiotic relationship between Asian savers and American spenders. One is that it gives the Asians leverage over the United States, in the conventional way that a creditor has leverage over a debtor. In the event of a disagreement over a foreign policy issue—the obvious examples that spring to mind are Taiwan and North Korea—the Chinese might consider reducing their exposure to U.S. bonds by selling a few billion off. That would apply pressure on the dollar and on U.S. interest rates. Yet this commonsense reasoning overlooks what such a strategy would cost the Chinese themselves. For the appreciation of their currency would immediately have an impact on their exports. It would also have a strong deflationary effect on their economy as a whole. And—more important, perhaps—it would inflict severe losses on Chinese institutions left holding dollar assets. Given the way Asian banks generally hold dollars in their reserves but lend long in their local currencies, dollar devaluation could punish the Chinese by tipping their banking system (which is far from healthy as things stand) into crisis.

57

The crux of the matter is that the Asian-American economic relationship is not symmetrical. Twentieth-century history handed the United States a privileged position in the world economy; its currency became and has remained the world’s favorite. Since 1945 it has been used more than any other for denominating international transactions, and that has made it the preferred currency for central bank reserves.

58

A century ago sterling enjoyed something of the same status. But sterling was strictly pegged to gold, just as the dollar was by somewhat different means during the years of the Bretton Woods system. De Gaulle complained in the 1960s that the United States was abusing its position as printer of the world’s reserve currency, but as long as the dollar retained the link to gold, there were limits to how far such abuse could be taken. Only from the 1970s onward, when the dollar became a pure fiat currency with its supply dictated by the Federal Reserve regardless of gold convertibility, was the United States really able to exploit the dollar’s unique appeal to foreigners. Ever since, the United States has periodically collected from foreigners the special tax known as seigniorage, the transfer from the holders of a currency to its issuer that automatically happens when the value of that currency is diminished. Dollar devaluations have been the device Americans have periodically used to reduce the real value of their external liabilities, most spectacularly in the mid-1980s. No other economy in the world reaps such benefits from devaluation as the United States. The cost in terms of more expensive imports is offset not just by the textbook stimulus to exports but, more important, by the real reduction in the value of America’s external liabilities.

It was not so long ago that the dollar fell precipitously on the world’s foreign exchange markets; it happened between 1985 and 1987. The second half of 2003 may have seen the start of a similar depreciation. Although the dollar’s real trade-weighted exchange rate has risen slightly, its nominal rate has already declined by more than two-fifths against the euro since February 2002. This raises an important question, touched on in the previous chapter: could the dollar’s reserve currency status be challenged by the euro? Recall that since the creation of the new European currency, international investors have acquired a whole new range of securities in which to invest, which are widely seen as being substitutes for dollar-denominated assets. Admittedly, the Eurozone economies seem to be stagnating compared with the United States by most measures of economic

performance. On the other hand, Europe has acquired the endearing characteristic of not wanting to fight wars, even when they are right on its doorstep. French and German leaders are also markedly less keen to confront Islamist extremists than their American counterparts. These things have their subtle benefits. For investors, the most important thing about a safe haven is, after all, that it should be safe.