Red Capitalism (5 page)

Authors: Carl Walter,Fraser Howie

Tags: #Business & Economics, #Finance, #General

Source: PBOC Financial Stability Report, various

Note: Interbank bonds include CGBs, financial bonds and all corporate bonds.

Over the course of 2003 and 2004, Zhou laid the ground work for his future policy initiatives. First, he actively shaped what became the first official government statement in support of China’s capital markets since Deng’s 1992 comments. In what became known as “The Nine Articles,” in early 2004, the Party emphatically affirmed the critical role of capital markets, which were defined to include the bond markets as well as the stock markets.

With this political cover in place, Zhou created the institutional infrastructure he would need to support bank reform. In September 2003, a new Financial Markets Department in the PBOC was established to lead the development of new policies and products for the bond markets. More strategically, on December 6, 2003, the PBOC established a wholly-owned corporate entity known as Central SAFE Investments (more commonly known as “Huijin”), and China Jianyin Investments, a wholly-owned subsidiary of Huijin. These entities became the crucial parts of the effort to restructure and recapitalize the Big 4 banks, channeling new capital to CCB and BOC in 2004. They also became the most fought-over piece of turf in the entire financial system.

Although Zhou’s starting point appeared to be banks and the underdeveloped bond markets, his real objective was the stock market. He knew well that bond risk continued to be borne largely by the banks and that only the stock markets truly enabled corporations to raise money directly from third-party investors outside of the banking system. To drive at a revival of the stock markets, however, was outside the scope of his jurisdiction; he would be stepping on other people’s toes. With the strong support of Jiang Zemin, who retained a place as chairman of the key China Military Commission until late 2004, as well as the help of the vice-premier in charge of finance, Huang Ju, Zhou began stepping on toes. Huang was another Shanghai holdover from the previous administration.

From early in 2005, the PBOC, working “closely” with other agencies (see

Table 1.3

), began implementing its plans for the bond markets, introducing a series of new initiatives one after the other. In February, rules came out permitting international institutions such as the Asian Development Bank to issue RMB bonds (“Panda Bonds”) and banks to establish mutual-fund companies as a first step toward a universal bank model. In March came regulations allowing asset-backed securities, and in May forward bond trading and a new corporate-debt product, commercial paper (CP), were introduced.

TABLE 1.3

Responsibilities for cross-regulatory financial reform

| Reform Initiative | Principal Responsible Entities |

| Panda Bonds | PBOC, MOF, NDRC |

| Bank business model: mutual funds subsidiaries | CSRC, CBRC |

| Asset-backed securities | MOF, PBOC, NDRC |

| Forward bond trading | PBOC, CBRC |

| Commercial paper (CP) | NDRC, PBOC |

| Bank recapitalization | MOF, PBOC |

| Failed securities company rescues | CSRC, PBOC |

| Exchange and interest-rate policy | PBOC/SAFE, MOF, Finance Small Group |

Functional bond markets without interest rates set by market forces cannot exist and these are to a significant extent related to foreign-exchange policy. Here, too, Zhou was successful. In June 2005, the PBOC was allowed to de-link the RMB from its fixed exchange rate to the US dollar and over the course of the next 18 months, the currency appreciated nearly 20 percent. In addition, in 2007, interest rates were increased in a single step by two percent in what was perceived as an initial step toward market-based rates. Taken together, the conditions for an active debt market were put in place. As a package, all these moves represented the most significant effort yet to stimulate the development of a bond market, but they paled in significance with what took place in the banking sector.

In 2004, both CCB and BOC had been recapitalized. Before receiving US$45 billion in new capital from the foreign-exchange reserves, the banks had written off their remaining bad loans. There followed the sale of stakes in both banks to international strategic investors. These investors played two roles. First, their investment confirmed to the international-investor community that the banks had been successfully restructured and now represented an attractive investment opportunity. Secondly, and equally important, these strategic investors were meant to partner with the two banks and upgrade all aspects of corporate governance, risk management and product development. In short, the objective of bank reform was to strengthen banks financially as well as institutionally so that Chinese bankers could offer sound judgment and advice. Instead of their saying “Yes!” and lending floods of money at the Party’s behest, Zhu Rongji hoped to create professional institutions that could help the government avoid the mistakes of the past.

In June 2005, Bank of America (BOA) acquired the right to purchase up to a 19.9 percent interest in China Construction Bank and in July, Temasek, one of Singapore’s sovereign-wealth funds, a further five percent. As a first step, BOA and Temasek respectively paid US$2.5 billion and US$1.5 billion for nine percent and 5.1 percent interests in CCB. This set off in the Chinese media an ugly bout of political mudslinging at the purported “sell-out” of valuable state banks to foreigners. The accusations derived from the viewpoint that China’s banks were now “clean,” since all bad loans had reportedly been stripped out. So, the argument went, if foreign investors were to be brought in, they should pay a high price to compensate the state for its losses. Aside from price considerations, even the notion of introducing foreigners itself led to accusations that the nation’s financial security was being threatened. This attack from the nationalist left came to encompass the entire bank-reform process. Despite such attacks, the PBOC was able to complete both the CCB and BOC restructurings and public IPOs as planned. But from 2005, the political environment changed and with it the character of the bank-reform initiative.

At the same time the PBOC, again acting through Huijin, had begun buying up bankrupt securities companies in the name of financial stability.

4

In the past, the central bank had provided what it called “coffin money” to compensate retail depositors in collapsed financial-sector entities. This time, however, its approach was different: it bought controlling equity interests in the failed securities companies. Over the course of the summer and fall of 2005, Huijin and its subsidiary, China Jianyin, acquired equity stakes in 17 securities companies—from the huge Galaxy Securities and Guotai Junan securities to smaller entities such as Minzu and Xiangcai. The PBOC’s expressed intention was to use a “market-based” approach. This meant that after restoring them to health, the bank hoped to recover its money by selling them off to new investors, and new investors would include foreign banks. From late 2004, the PBOC had put a 51 percent stake in a medium-size, bankrupt securities company up for bid among interested foreign banks. One bank had won the bidding process and a full proposal had been sent to the State Council for approval in the early summer. Zhou’s intention was to throw the entire domestic stock market open to direct foreign participation for the first time.

China has been said to have created and perhaps perfected over the millennia the art of bureaucracy. The PBOC and Zhou Xiaochuan, in the course of 2004 and 2005, seemed to have violated every norm of traditional bureaucratic behavior. The bank reforms wiped out Ministry of Finance (MOF) investments in CCB and BOC, and the corporate-debt space of the National Development and Reform Commission (NDRC) was invaded by allowing securities firms and SOEs to issue short-term debt securities. They were trying to blast open the CSRC’s territory by selling majority control of a securities company to a foreign bank. In the press, it was beginning to be said of Huijin that it was the “Financial State-owned Assets Supervision and Administration Commission (SASAC).” Even worse, the PBOC was making the case for establishing a Super Regulator that would integrate oversight of the bank, equity, and debt-capital markets under one roof. Suddenly, ugly personal attacks, which clearly emanated out of Beijing, were being made on Zhou Xiaochuan in the Hong Kong press.

A ministry-level entity such as the PBOC can only succeed against a concerted attack from many of its peers in the State Council if it has the full support of the country’s top leadership. Jiang Zemin had retired early in the year, and it was unfortunate that in the late summer of 2005, Vice Premier Huang Ju was diagnosed with terminal cancer; a key ally was lost. It was almost inevitable, therefore, that during the October National Day holidays of 2005, the State Council began to cut Zhou Xiaochuan’s initiatives down to size, restoring balance across the bureaucracies. After the holiday period, it rapidly became clear that the MOF had recovered influence over the banks, that the CSRC had succeeded in stopping majority-controlled foreign entry into its market, and that the NDRC’s authority had been enhanced. Even the heavily pro-PBOC

Caijing magazine gave the head of the NDRC a front-page cover story. The results reverberate to this day: an integrated approach to financial reform had ended. What followed has been piecemeal and limited to within the silos of authority belonging to each separate regulator.

magazine gave the head of the NDRC a front-page cover story. The results reverberate to this day: an integrated approach to financial reform had ended. What followed has been piecemeal and limited to within the silos of authority belonging to each separate regulator.

From 1998, Zhu Rongji and Zhou Xiaochuan had built up a certain framework to pursue comprehensive reform of the financial markets. This included the creation of bad banks, the strengthening of good banks, a national social-security fund, bond markets with a broader investor base and, last but not least, stock markets open to meaningful foreign participation. In addition, there was a start to currency reform as the RMB was unlocked from its link to the US dollar. After the PBOC’s defeat in 2005, this institutional framework remained incomplete. Worse still, it has been, and continues to be, used to solve problems it was never meant to address. The reason for this is relatively straight forward: with the RMB exchange rate from early 2008 again locked in to the US dollar, interest rates and markets have been frozen in place.

5

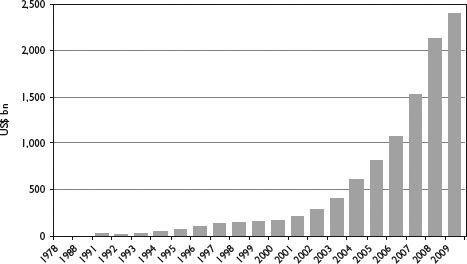

The dollars poured in (see

Figure 1.8

), creating massive amounts of new RMB and huge pressures within the system. Lacking an integrated set of policies, the government addressed these pressures with a plethora of

ad hoc

institutional, administrative and other adjustments reached by consensus decision making and compromise. The result by 2010 is a jerry-built financial structure caught somewhere between its Soviet past and its presumably, but not assuredly, capitalist future.

FIGURE 1.8

China’s foreign-exchange reserves

Source: China Statistical Yearbook 2008

CHINA IS A FAMILY BUSINESS

What is remarkable about the financial reforms pursued by Zhu Rongji was that they were comprehensive, transformational, and pursued consistently. Failure to follow through may have been inevitable, however, given the fragmented structure of the country’s political system in which special-interest groups co-exist within a dominant political entity, the Communist Party of China. What moves this structure is not a market economy and its laws of supply and demand, but a carefully balanced social mechanism built around the particular interests of the revolutionary families who constitute the political elite. China is a family-run business. When ruling groups change, there will be an inevitable change in the balance of interests; but these families have one shared interest above all others: the stability of the system. Social stability allows their pursuit of special interests. This is what is meant by calls for a “Harmonious Society”.